Finding a good place to park your savings shouldn’t feel overwhelming. That’s why we publish regular rankings of the best savings accounts, money market accounts, and certificates of deposit (CDs) available to everyday consumers in the U.S.

Our goal is simple: help you find accounts that pay the highest interest rates, without forcing you to dig through fine print or marketing claims. Below is a plain-English explanation of how we research accounts, decide which ones qualify, and rank them.

How We Search for the Best Rates

We track deposit accounts from roughly 200 banks and credit unions across the country. This includes both traditional brick-and-mortar banks and online-only institutions.

From this group:

-

About 200 offer CDs that meet our standards

-

Around 100 offer high-yield savings accounts

-

About 60 offer money market accounts

Our team reviews rates every business day, using a mix of automated tools and hands-on checks. Banks often update their rates in the morning, but changes can happen throughout the day, so we monitor continuously to keep information fresh.

If a bank expands nationwide or a new online bank launches, we add it to our tracking list as soon as it qualifies.

Which Banks and Credit Unions Are Included?

To appear in our rankings, financial institutions must meet two basic requirements.

1. Your Money Must Be Federally Insured

Safety comes first. We only include:

-

FDIC-insured banks, or

-

NCUA-insured credit unions

This means your deposits are protected by the U.S. government up to $250,000 per person, per institution, in case the bank or credit union fails.

Online banks are treated the same as physical banks. If they’re FDIC-insured, your money is just as safe.

2. The Account Must Be Available Nationwide

Our rankings are designed for readers across the U.S., so we only include institutions that accept customers from most states.

-

Most banks we list serve all 50 states

-

Some serve at least 40 states (these exceptions are clearly noted)

Credit unions work a bit differently. Many require membership based on location or employer. However, some allow nationwide membership through simple steps, such as joining an affiliated nonprofit.

We explain any membership requirements clearly and exclude credit unions that require large upfront fees to join.

Which Savings and Money Market Accounts Qualify?

For savings accounts and money market accounts to be included:

-

The minimum balance to earn the top rate must be $25,000 or less

-

The account must allow free withdrawals or transfers, aside from standard fees like wire transfers or out-of-network ATM fees

-

If the account is mobile-only, the app must work on both iOS and Android

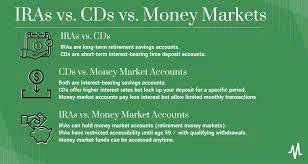

Savings vs. Money Market Accounts

We classify accounts based on how they actually work:

-

Savings accounts: No check-writing

-

Money market accounts: Allow check-writing

Some banks use “money market” as a marketing label, even when checks aren’t allowed. In those cases, we classify the account based on features, not the name.

Which CDs Qualify?

Certificates of deposit must meet specific rules to be ranked:

-

Standard CDs: Minimum deposit of $25,000 or less

-

Jumbo CDs: Minimum deposit between $50,000 and $100,000

We don’t rank “super jumbo” CDs that require $250,000 or more, since they’re rare and not widely available.

Rate Structure Matters

To qualify, a CD must:

-

Have a fixed interest rate for the entire term

We exclude:

-

Variable-rate CDs

-

Indexed CDs tied to unpredictable benchmarks

One exception: bump-up CDs, which allow you to increase your rate once during the term. Since the original rate is guaranteed and the bump can only help you, we include them.

What Automatically Disqualifies an Account?

Some accounts look attractive at first glance but don’t pass our standards.

We exclude accounts that:

-

Pay the top rate only on very small balances (under $5,000)

-

Advertise teaser rates that apply to limited amounts

-

Charge fees just to move your money out

Updated Savings Account Rules

As of April 2025, we expanded our criteria to give readers more choices. Savings accounts that require:

-

Direct deposit, or

-

Opening a linked checking account

can now qualify. These requirements are clearly disclosed so you can decide if the account fits your situation.

How We Rank Accounts Once They Qualify

Savings and Money Market Accounts

Accounts are ranked by:

-

Highest APY (interest rate)

-

Lowest balance required to earn that rate

-

Lowest opening deposit

-

Alphabetical order (if still tied)

Certificates of Deposit (CDs)

CD rankings follow a similar process:

-

Highest APY

-

Shortest term length (within the same category)

-

Lowest minimum deposit

-

Alphabetical order

We group CDs by term ranges (for example, CDs close to one year are ranked together), since many banks offer non-standard term lengths.

Choosing the Right Account for Your Situation

A top interest rate can make a big difference over time. Choosing a higher-paying account instead of an average one could earn you hundreds or even thousands of extra dollars.

That said, the “best” account isn’t always the one with the absolute highest rate.

You might:

-

Prefer a bank you already use

-

Want a shorter CD term

-

Avoid institutions you’ve had issues with before

-

Choose a bank over a credit union (or vice versa)

That’s why our rankings usually include 15 or more strong options for each product. Every account listed is among the top-paying choices nationwide — the final decision depends on what works best for you.

The Bottom Line

Our rankings are designed to cut through the noise and help you quickly find safe, high-paying places to store your money. We focus on interest rates, accessibility, and fairness — not advertising relationships.

Whether you’re building an emergency fund, saving for a goal, or locking in a CD rate, our process is built to give you clear, trustworthy options so you can make confident financial decisions.